Adding A Cash Position

Adding A Cash Position

Last week we introduced the concept of an efficient frontier. This set of portfolios creates a curve in the return vs. risk space that sometimes resembles a rocket taking off from the ground and bending toward orbit. It seemingly asymptotes to a nearly linear reward for risk trade-off at the upper ranges of typical asset class annualized risk measurements. This week, we added one layer of complexity by adding a cash position to our traditional two asset (bonds and stocks) portfolio. A cash position can help us reduce our risk or increase our expected returns for most expected risk levels.

Source: JQR Capital

The Market Portfolio

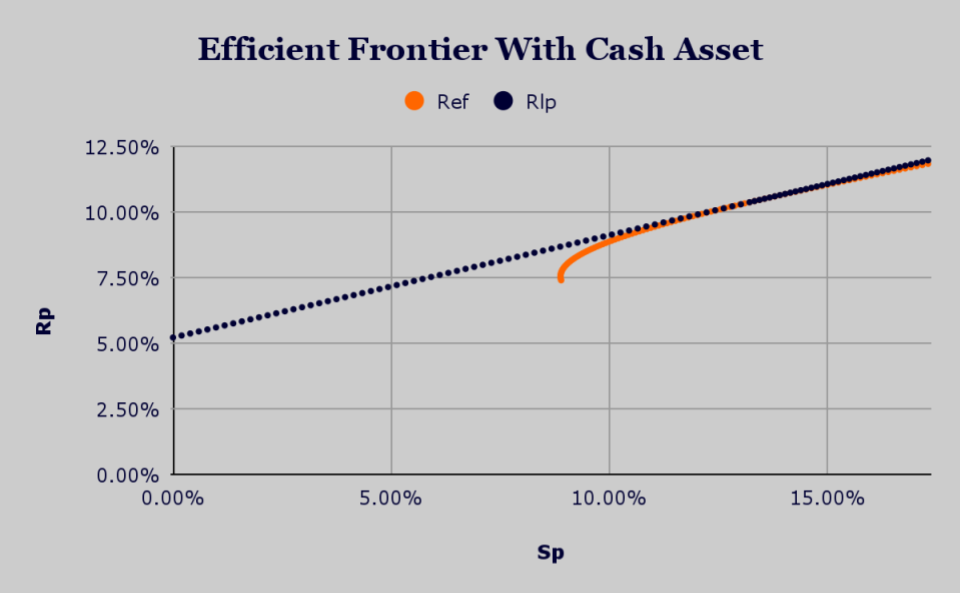

The easiest way to visualize adding cash to our set of bond and stock portfolios is to plot the expected interest yield on a cash asset along the y-axis of our return vs. risk space. We then imagine a vertical line “falling” from that pivot point down onto our now familiar efficient frontier of bond and stock portfolios. The landing point is defined mathematically as a tangency point marked by the bond plus stock portfolio on the efficient frontier with the highest Sharpe ratio. The Sharpe ratio is defined by the following formula.

SR = (Rp - Rf) / (Sp - Sf)

Where the return and risk of the portfolio are defined by Rp and Sp. We also introduce the concept of a “risk free” rate as a more technical term for our cash asset. It is often assumed that this risk free rate has a risk of 0.00% - which is why we plot the cash interest yield along the y-axis. An important enhancement to this framework is the labeling of the tangency point as something called the “market” portfolio (MP). Many investment banks (the Goldman Sachs’ and Morgan Stanley’s of the world) used to publish their market portfolios around this time of the year and label them as their strategic allocations for the next investing cycle.

Source: JQR Capital

To Lever Or Not To Lever?

Adding a cash position to the efficient frontier (ef) of bond and stock portfolios introduces an interesting dilemma for some investment managers - to lever or not to lever? Most retail and institutional investors are what are described as “long only” - meaning they are not allowed to use what is called leverage when constructing investment portfolios. By allowing leverage, we can construct a levered portfolio (lp) that differs from our standard efficient frontier. In looking at the chart shown above, we label two specific regimes along the straight line connecting us to the cash position: 1. Lending (by investing in cash) and 2. Borrowing (by leveraging the market portfolio). In this case, the borrowing portion of the line is very close to the bond and stock efficient frontier. Hedge funds are usually the only investment managers allowed to use this borrowing technique because they cater to what are called accredited investors.

Source: JQR Capital

The Risk Free Rate

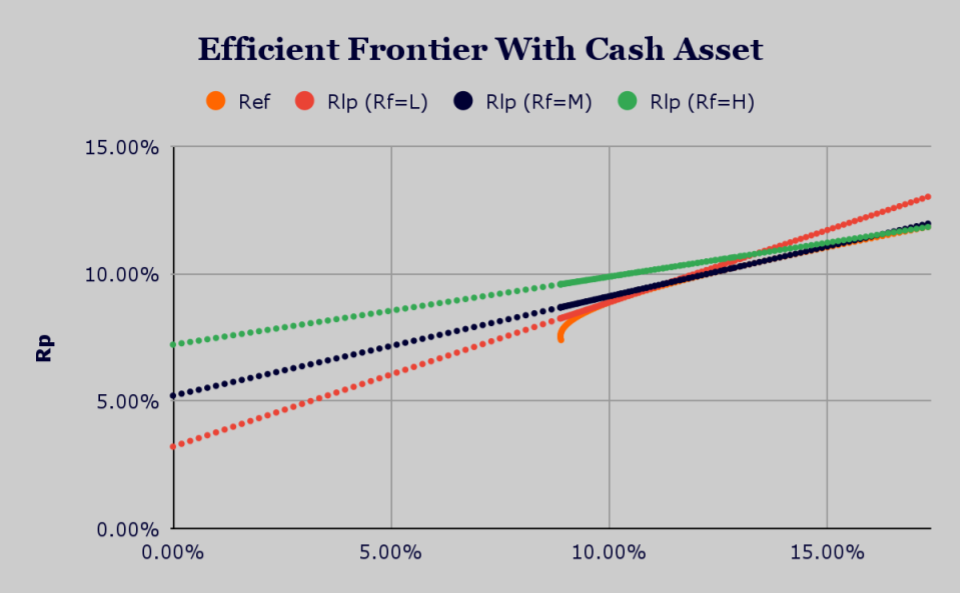

The last complexity we will discuss this week is this whole idea of the risk free rate. There are countless ways to think of this cash position. It can be as simple as the interest rate you receive in your savings account at the neighborhood bank. It is most often thought of as the current interest yield on the shortest term US Treasury. One nuance of this risk free rate is that when it changes, the tangency - or market - portfolio changes in the balance of bond allocation to stock allocation. The chart shown below illustrates the effect on this balance with a lower risk free (3.21%) rate, a medium risk free rate (5.21%), and a higher risk free rate (7.00%). A lower risk free rate leads us to a higher bond allocation in our market portfolio while a higher risk free rate leads us to a higher stock allocation in our market portfolio.

Source: JQR Capital

JQR Capital offers you a complimentary one hour consultation to “Find Your Bearings” in your lifelong voyage to find your own private island. Please click the link shown below.

Disclaimer

Past performance is no guarantee of future results. Any investment involves some amount of risk and may not be suitable for all — or any — individuals. You should consult with your investment advisor before acting on this — or any — financial information.

References

https://www.investopedia.com/terms/s/sharperatio.asp

Copyright © JQR Capital Management, LLC 2024

Comments

Post a Comment