Are Multiple Factors Better?

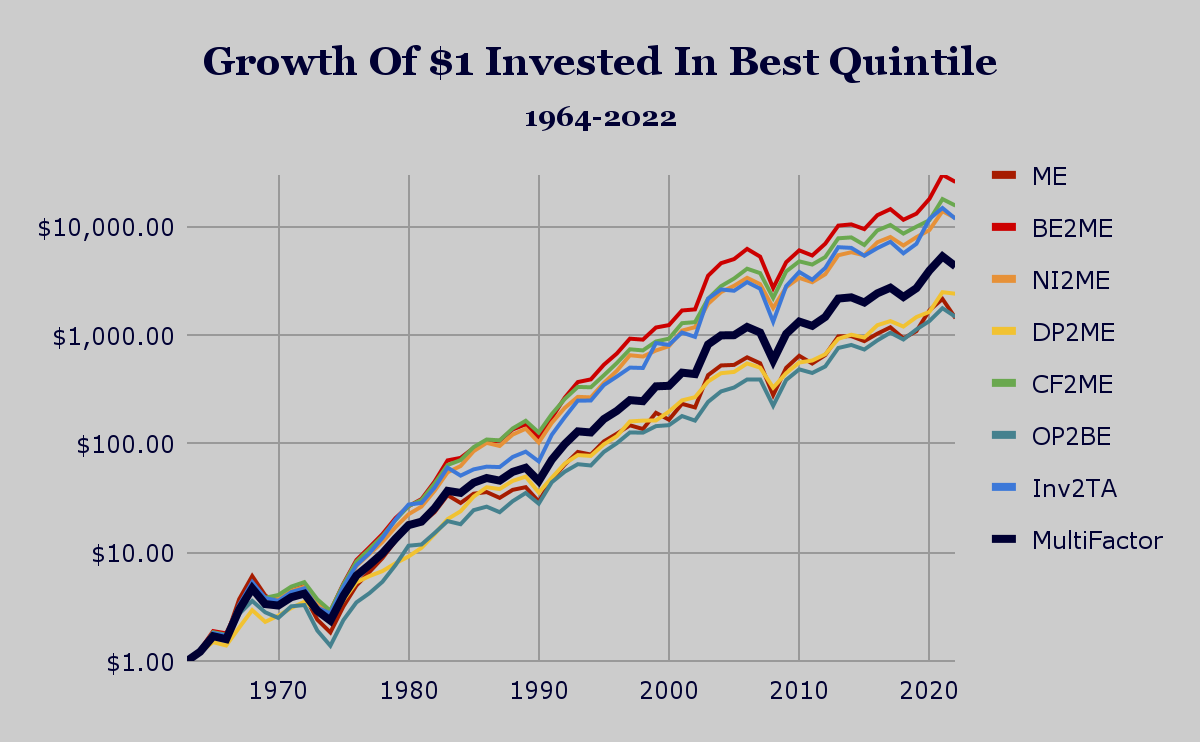

Source : Ken French Data, JQR Capital calculations Are Multiple Factors Better? Two weeks ago we looked at the idea of combining more than one factor into a multi factor model portfolio. We calculated and presented a correlation matrix showing the average annual correlation between the slopes of the factor payoffs. In this post, we look not at the slopes of the factor payoffs, but of the return streams from investing in just one of the fractiles. We will utilize the best quintile for each factor. This was the smallest quintile (Q1) for the market equity (ME) and investment divided by total assets (Inv2TA) factors. For the other five factors, the best quintile was the highest (Q5). As a reminder, here is the growth of $1 from 1964 to 2022 for ME Q1. Source : Ken French Data, JQR Capital calculations This chart shows the ME factor grew from $1 invested at the beginning of 1964 to $1,420 at the end of 2022. This growth pattern was not all peaches and cream with steep losses in 1968 to 197...