Are We There Yet?

Are We There Yet?

When my kids were young, they would always ask: “How much longer?” My standard answer was: “5 more minutes.” After many of these exchanges, I would respond with: “6 more minutes” and then “7 more minutes.” They finally figured out that I really had no idea how much longer. This week we try to answer the economic question: “Are we there yet?”

From an investing perspective, I think we are currently in a “Goldilocks” moment for three reasons: (1) inflation has seemingly been tamed to provide price stability, (2) unemployment rates are near all-time lows, and (3) the economy continues to expand. We are long term investors who employ a strategic asset allocation that assures our clients are always "in" the market. We do not believe that a market timing approach works well for anyone who cannot accurately forecast the future (translation: all mere mortals). We will discuss this in detail in our blog next week.

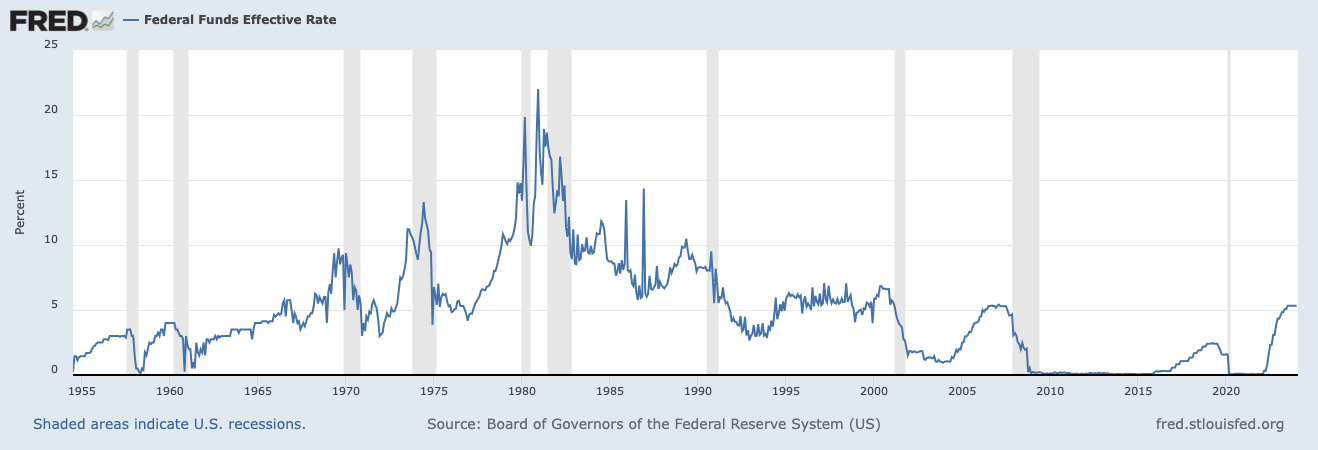

Last week we introduced a cash position to our efficient frontier and gave it a technical term: the risk free rate. This idea has a very deep meaning that we will uncover in this post. As you may know, interest rates had been rock bottom for several years after the 2008 financial crisis and then again during the early days of the COVID-19 outbreak. They then began to rise dramatically as we emerged from the pandemic panic and started to spend money again. The chart shown below illustrates this recent surge in the federal funds overnight rate. The gray shaded bands indicate dates of recession - or quarters with negative gross domestic product.

Source: Federal Reserve Bank Of St. Louis

Federal Open Market Committee

The Federal Open Market Committee (AKA the FOMC or The Fed) meets eight times per year. These meetings are held just before and just after the end of each calendar quarter to discuss the state of the US economy and what - if any - policy decisions need to be made to fulfill their dual mandate. The dual mandate is to provide price stability and full employment. These two goals are truly a balancing act because as unemployment rates drop, there are more people employed. When there are more jobs than workers, those workers have the flexibility to seek higher pay with their current employer or jump ship for greener pastures. The potential increase in pay translates into increased demand for goods and services - thus pushing prices higher in the form of inflation.

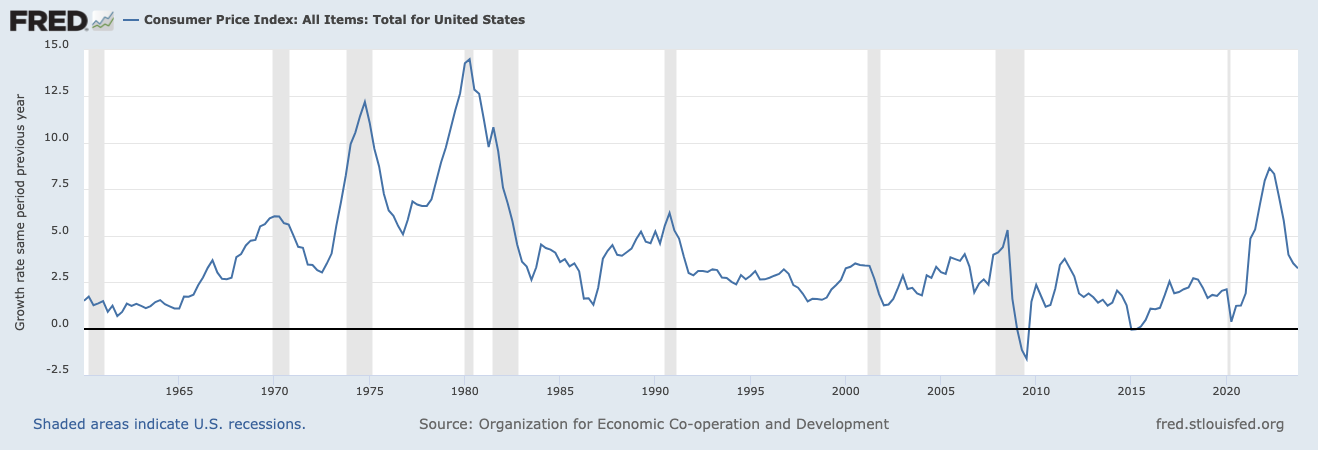

Source: Federal Reserve Bank Of St. Louis

The chart displayed above shows the inflation rate history since 1960. Price spikes in the late 1970s were vivid reminders of the energy crisis when many of us learned to carpool around town and wear sweaters at home. We can see the recent increase in inflation and the very recent drop down closer to the FOMC target rate.

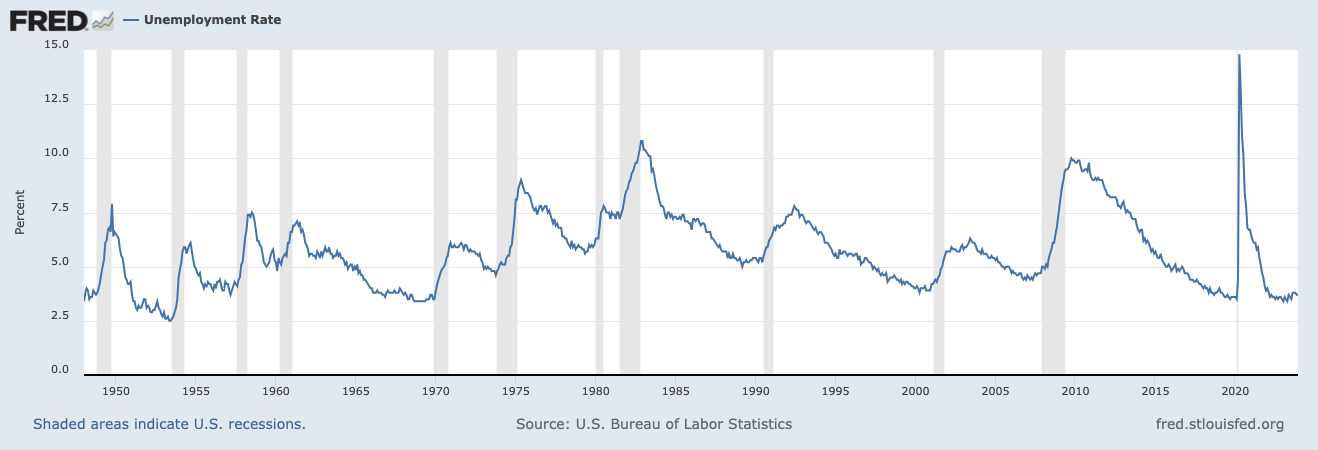

The unemployment rate is charted below from the 1940s. The COVID-19 outbreak put many leisure services (hotels, airlines, and restaurants) employees not out on the street, but back home on their couches. The current unemployment rate is once again hovering close to all time lows. Now may be a good time to consider a jump!

Source: Federal Reserve Bank Of St. Louis

Who Should Pay Attention?

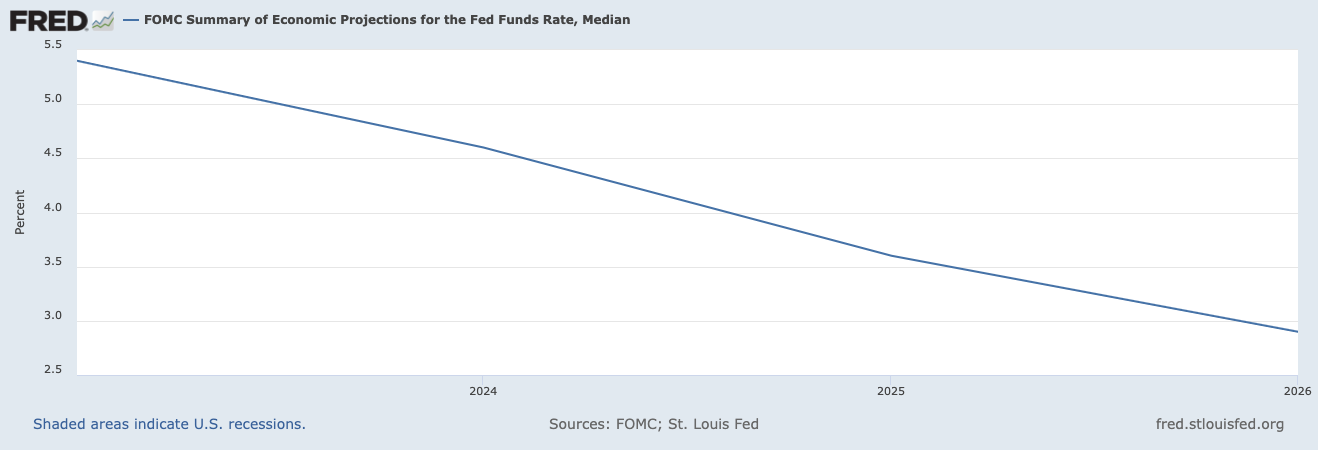

In one word: EVERYONE. The federal funds overnight rate is the lowest risk interest rate on the planet. It is the basis of all treasury rates, all mortgage rates, and all corporate rates in the fixed income world. Movements in the fed funds rate affect virtually every aspect of our global economy and provide important signals from the FOMC regarding our economic future. The chart shown below is about one year old, but it shows the intended glide path of short term interest rates into early 2026. As expectations for inflation settle down to (or below) the FOMC target of 2%, we should expect interest rates to mirror their decline. This would encourage lending and risk taking for the private sector.

Source: Federal Reserve Bank Of St. Louis

It is [a good thing] that people of the nation do not understand our banking and monetary system, for if they did, I believe there would be a revolution before tomorrow morning. - Henry Ford

JQR Capital offers you a complimentary one hour consultation to “Find Your Bearings” in your lifelong voyage to find your own private island. Please click the link shown below.

Disclaimer

Past performance is no guarantee of future results. Any investment involves some amount of risk and may not be suitable for all — or any — individuals. You should consult with your investment advisor before acting on this — or any — financial information.

References

https://research.stlouisfed.org/

Copyright © 2024 JQR Capital Management, LLC

Comments

Post a Comment