Portfolio Construction 101

Source: Alex Lang

Portfolio construction is the science (and art) of combining macro asset allocation strategy with the micro security selection tactics. Just like building a house or a boat, many times the "devil" is in the details. What may look simple and elegant from the outside may be fraught with challenges when we pull back the cover.

Expected Returns

Estimating security returns is the most important part of the portfolio construction process. While there are countless techniques and a maze of details, there are three main ways a fundamentalist can estimate an expected return for portfolio candidates. These are listed below in the ascending order of complexity.

- Capital Asset Pricing Model (CAPM)

- Relative Value Models

- Intrinsic Value Models

As the name implies, relative value models attempt to compare individual securities to each other or to a market benchmark using one (or more) metrics. Comparing these metrics may provide insights into which securities are poised to outperform a benchmark (such as the S&P 500) and which ones may be ready for a spell of lousy returns. Some of the metrics that may exhibit explanatory power in predicting future security returns are: return on equity (ROE), price to sales ratio (P/S), price to earnings ratio (P/E), price to book ratio (P/B), and dividend yield (D/P). The example for AAPL is E(RAAPL) = Net IncomeTTM / Market Capitalization = $57,411,000,000 / $2,084,000,000,000 = 2.75%. This is one way to estimate an expected return over the next 12 months for AAPL. The chart below shows the expected returns using this very simple relative value model for the constituents of the S&P 500.

Expected Risks

Various risk measures are used in an attempt to quantify what can go wrong for any one (or a market) investable security. The most common measure of risk is the standard deviation of historical returns. There are two components of this measure: market risk and stock specific risk. These two are sometimes called systematic risk and unsystematic risk. Unsystematic risk (Su) can be diversified by adding additional securities to a portfolio, while systematic risk (Ss) is an underlying risk of the market. The chart below shows the theoretical convergence of total risk to just the systematic component as we approach 500 constituents in the S&P 500.

Expected Correlations

Just because an investment security is of the same type (bonds, stocks, other), does not mean that their return patterns are very similar. Conversely, investment securities who "should" be less correlated often have less diversification value than we might expect looking in from the outside. The table below indicates that the Treasury bond ETFs (SHY, IEF, and TLT) are all highly correlated as warned by their red color format. Green colored cells point us toward portfolio candidates whose uncorrelated return patterns could help "smooth" the ride for our portfolio into the future.

Transaction Costs

Transaction costs are what make the portfolio construction process most interesting. The best strategies in the world can look great on paper, but when we put them to work with real money we may be disappointed by the final results. This is (partially) because transaction costs - and taxation effects - can make it very difficult to outperform an investment strategy implemented using exchange traded funds tracking passive indices. There are two main types of transaction costs that we need to estimate in the portfolio construction process: explicit and implicit.

Explicit Transaction Costs

Explicit transaction costs are easy to calculate and do not vary according to the size of our position. They may be a $4.95 charge for each trade executed by our broker. Some transactions are priced on a per share basis - making trades of lower priced securities very expensive when compared to higher priced shares for the same dollar value on a trade. The recent "race to zero" has many investors now paying a commission of exactly $0.00. We know that nothing comes for free and the implicit transaction costs can help the brokerage firm generate revenue and cost us money in our portfolios.

Implicit Transaction Costs

Implicit transaction costs are more difficult to estimate and may vary depending on market conditions, position size, and trader habits. A bid-ask spread is simply the difference between the price the buyer is hoping to pay and the price the seller is hoping to pocket. For actively traded securities this is very small in proportion of the share price. For less "liquid" securities, the spread can be quite wide. Market impact is the dynamic of price movement that occurs when a trade is placed into the market. A large order to buy a security can cause the price to move upward, while a large order to sell that same security can cause the price to move downward. Estimating the market impact. of a trade is a bit like Heisenberg's Uncertainty Principle in that in order to measure the impact, we alter the effect of the impact. The final implicit transaction cost is trader delay. This is the indecision by a trader in the hope that they may transact at a more favorable price later in the day, week, month, quarter, or year. When their intended trade is not filled, it is referred to as opportunity cost.

- Bid-ask spread

- Market impact

- Trader delay

Together, these three implicit transaction costs represent the hidden portion of an iceberg that lies below the surface of the water. Their combined effect can literally sink a portfolio that either invests in highly illiquid securities or employs a frequent trading schedule.

Source: National Ocean Service Image Gallery

Optimization

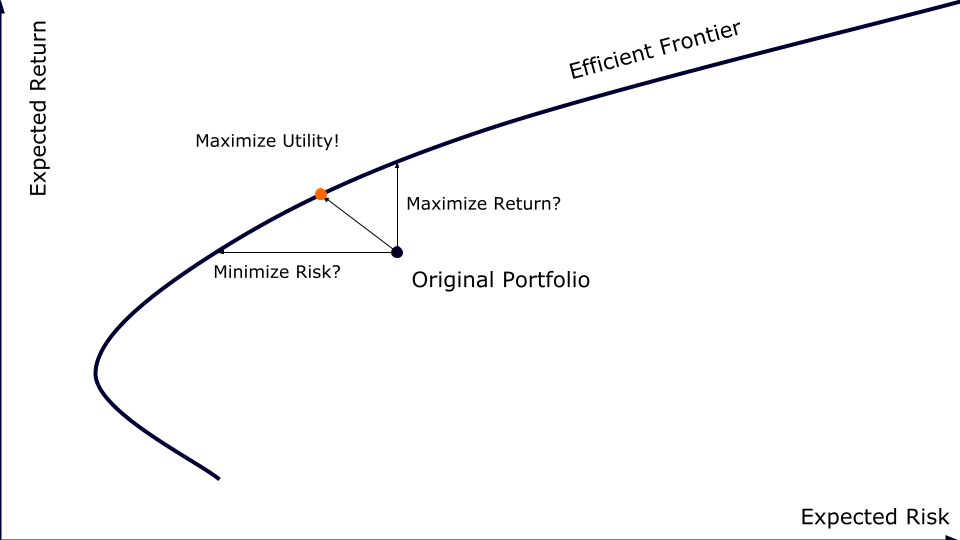

Optimization is the final step in portfolio construction before uploading a trade list to a broker. This process takes all the inputs mentioned above and provides an optimal weighting of all security candidates that will perform one of three different functions:

- Minimize the expected risk for a desired expected return,

- Maximize the expected return for a desired expected risk, or

- Maximize the expected investor "utility" based on their own individual risk tolerance.

The idea of investor utility deserves a brief explanation. In the equation below, we can estimate utility of a portfolio (Up) as the expected return of the portfolio, E(Rp), minus half the risk aversion (RA) multiplied by the expected portfolio variance - or E(Sp)2. A "risk neutral" investor will have an RA of 0 and can be thought of as a robot. A very risk averse investor might have an RA of 10 and will be very reluctant to take any risk.

Up = E(Rp) - 0.5 * RA * E(Sp)2

An average investor whose RA is 5 shows that typically investors feel 2.5 times more "pain" from their losses than they feel "glee" from their gains. This crude diagram helps us visualize the three main ways that optimization can help us in the portfolio construction process.

Each of these topics is a can of worms that we will explore in future discussions. Past performance is no guarantee of future results. Stay tuned!

Comments

Post a Comment